For millions of Americans, Social Security is a cornerstone of their retirement income. But did you know that only 4% of retirees claim their benefits at the optimal time? That means 96% of people are leaving money on the table. This could potentially add up to tens of thousands of dollars over their lifetime.

Getting a better understanding of the ins and outs of Social Security can make a big difference in your financial future. Whether you’re retiring soon or just planning, here’s what you need to know about maximizing your Social Security benefits in 2025.

Wait…What About the Future of the Program?

Without new legislation, by 2035 the Social Security Trust Fund is projected to be depleted. But that doesn’t mean the program will disappear. Payroll taxes will still fund about 83% of scheduled benefits. However, as more Baby Boomers retire, the system will remain under pressure.

Planning ahead is more critical than ever. Social Security was designed to replace about 40% of pre-retirement income, but your personal percentage depends on your earnings history and when you claim benefits.

How Inflation Affects Your Benefits

Social Security benefits adjust annually to keep pace with inflation, thanks to the Cost-of-Living Adjustment (COLA). In 2025, COLA is set at 2.5%, one of the smallest increases in recent years.

What does this mean for retirees? The average monthly benefit will rise from $1,927 to $1,975, an increase of just $48. This adjustment is unlikely to fully keep up with rising costs, reinforcing the need for additional retirement income strategies.

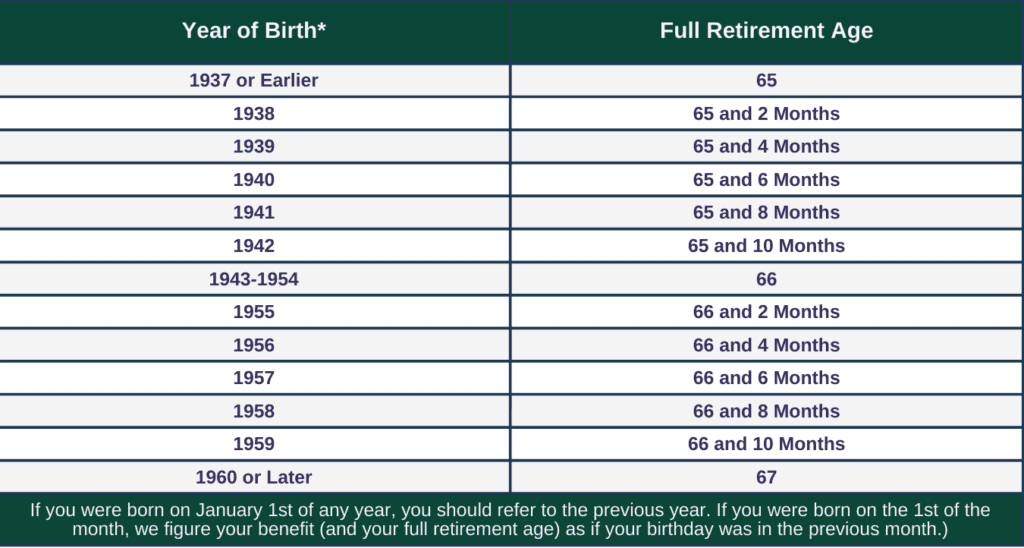

Know Your Full Retirement Age (FRA):

While you can claim Social Security as early as age 62, doing so results in permanently reduced benefits. Your full retirement age (FRA) depends on your birth year:

- If you were born before 1960, your FRA is between 65-66.

- If you were born in 1960 or later, your FRA is 67.

Waiting until your FRA ensures you receive 100% of your benefit, while claiming early could reduce it by up to 30%.

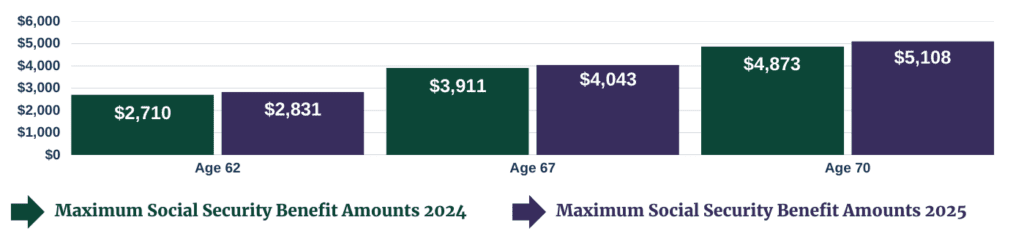

Delaying Until Age 70 Could Really Pay Off…

Every year you delay past your FRA (up to age 70), your benefits increase by 8% per year. Here’s an example:

- If you retire at 62 in 2025, your maximum monthly benefit would be $2,831.

- If you retire at 67, it jumps to $4,018.

- If you delay until age 70, your maximum benefit reaches $5,108.

That’s a huge difference—especially if you spread it out over a 20-30 year retirement!

Keep Working to Boost Your Benefit

Social Security calculates your benefit based on your highest 35 years of earnings. If you continue working in your 60s and replace your lower-earning years with higher-earning ones, your benefit can increase.

Keep in mind, however, if you claim before your FRA and keep working, there is an earnings limit.

In 2025:

- If you’re under FRA, you lose $1 in benefits for every $2 earned above $23,400.

- The year you reach FRA, you lose $1 for every $3 earned above $62,160.

- Once you hit FRA, there’s no earnings limit.

Maximize Spousal and Survivor Benefits

Are you married, divorced, or widowed? You may qualify for additional Social Security benefits.

- Spousal Benefits: If you’re married, you can claim up to 50% of your spouse’s FRA benefit.

- Divorced Benefits: If you were married for at least 10 years, have been divorced for at least 2 years, and remain unmarried, you can claim benefits based on your ex-spouse’s record.

- Survivor Benefits: If your spouse passes away, you may be eligible to receive their full benefit instead of your own.

Timing matters—so work with an advisor to determine the best strategy.

Changes to Social Security in 2025

Several key updates are in place this year:

- The maximum taxable earnings limit rises to $176,100, meaning higher earners will pay more in Social Security taxes.

- Work credit earnings increase—you now earn one credit for every $1,810, up to four credits per year.

- Social Security statements are now mostly online, so set up your My Social Security account to check your earnings and benefit estimates.

Create a Plan That Works for You

Social Security is complex, but the right strategy can maximize your lifetime benefits. Every retiree’s situation is unique—your health, longevity, work plans, and financial goals all play a role in determining when and how to claim.

Need help optimizing your Social Security strategy? MoneyLetter’s sister company Asset Strategy is here to guide you. Every question is important. Let’s ensure you get every dollar you deserve.

If you need financial advice or a financial review, we would be happy to introduce you to a licensed advisor at our sister company, Asset Strategy Advisors (ASA). ASA is an SEC registered investment advisor. Contact us, or click HERE, to learn more.

https://assetstrategy.com/moneyletter-managed-account-program

Read some of our other blogs!

References:

4. https://www.ssa.gov/faqs/en/questions/KA-01951.html as of 10.10.2024

5. https://www.ssa.gov/cola/ as of 12.31.2024

7. https://www.ssa.gov/oact/cola/cbb.html as of 12.31.2024

8. https://www.ssa.gov/oact/cola/examplemax.html as of 12.31.2024

11. https://www.ssa.gov/news/press/factsheets/colafacts2025.pdf as of 10.9.2024

13. https://www.ssa.gov/pubs/EN-05-10072.pdf as of 11.27.2024

15. https://www.ssa.gov/oact/cola/sga.html as of 12.31.2024

Disclosure: The information provided in this blog is for informational and educational purposes only. MoneyLetter® does not purport to provide legal, tax, or individual investment advice. While carefully screened, the accuracy of the statistical data in MoneyLetter® cannot be guaranteed. Past performance does not ensure future results. All investments carry risks, including the loss of principal. Readers should carefully review investment prospectuses before investing.